Problem

In Denmark, young adults are struggling with a difficult financial challenge. One in five young Danes finds themselves under financial distress, which not only diminishes their life satisfaction but also hampers their ability to thrive. Organizations including OECD and the European Union have highlighted an urgent need to boost both financial literacy and digital financial literacy among citizens to better equip them for the complexities of modern financial life.

Approach

To help address the challenge, our team of three Digital Design students adopted a Research Through Design approach. From interview insights we created design provocations (lo/mid-fi design concepts in Figma). We explored these design openings with young adults in order to gain insights into what might motivate them to become financially literate. From these rich insights we created three in-depth digital concepts that we tested with young adults. Following these iterations we presented design guidelines that might help inform future designers on how to foster meaningful motivation digitally for young adults in their journey towards financial literacy

"How can digital design be utilized to motivate young adults in attaining financial literacy?"

Design process

Interview personas

Magnus has an interest in personal finance reflected in his hobbies.

He is passionate about investments.

He writes articles for a Danish investment publication

He helps other young people on online forums

He has a detailed overview over his personal finances

He plans ahead and saves for his retirement

He does not want any financial tool to be entertaining. He prioritizes utility.

Lasse, 25

The free-spirited young adult

Lasse prioritizes living in the moment and often spends money on nights out with friends.

He often regrets his spending the next morning

Lasse is extremely short-term focused, primarily aiming to make his salary last the month and pay rent.

He has knowledge of budgeting and financial sense from home but lacks the self-discipline to follow it.

Lasse connects poor mental well-being with a bad financial situation.

Expert interviews

We interviewed two educators that teach young adults in personal finances. One was employed by a well-known Danish bank. The other was from a non-profit organization teaching high school students in financial literacy. The most prominent finding was that learning subjects should be relevant to them in their current life situation. If the content does not relate to the students' current life situations it results in worse engagement and less willingness to learn about financial concepts.

Design ideas

WIth our initial research findings, we utilized the 6-3-5 sketching method for brainstorming, generating 18 different ideas to inspire ways our informants could become motivated in gaining financial literacy. To ensure our test sessions remained within a reasonable time frame, we established design criteria to help us narrow down which ideas were the strongest:

The idea must have a distinct function or concept – the provocation should be easily understood by the viewer.

The idea must be evocative – the provocation should prompt reflection on a future with use of the digital concept.

The idea must address one or more aspects of Self-Determination Theory (SDT): autonomy, competence, relatedness, or extrinsic motivation.

In the end we chose 7 diverse ideas to pursue with rapid prototyping in Figma, in order to test with high-schoolers and university students.

Insights from testing the design ideas

Social responsibility and relatedness with digital avatars

This theme relates to one of our design provocations, that explored how the young adults would feel about losing autonomy over their personal finances to an AI that decides what they can or cannot buy. We found that a complete loss of autonomy was not ideal, but a digital tool that guided them could be valuable.

"What if instead of blocking the purchase completely, you get a notification on your phone that says: 'Hey, we can see that you're buying this. You're already 200 DKK over budget'. That's nudging instead".

Rewards can motivate

In both studies, informants expressed that they would be motivated by receiving monetary rewards for their financial performance

"Even if it's only 2.31 DKK, you're like: 'oh well, I've won something anyway. Okay 2 DKK, but it's still the feeling of free money".

Relatability to life situations can motivate

Opportunity solution tree

We arranged the research insights with the seven design provocations in an Opportunity Solution Tree to organize how our findings related to the different psychological needs from motivational theory: Autonomy, competence and relatedness. In this way, we considered these three psychological needs as opportunities to contribute to our desired outcome - to create motivation for financial literacy.

After arranging the different themes, we brainstormed how they could be combined and conceptualized into specific concepts and to what extent they could support specific financial literacy topics. These could be all from budgeting to learning about financial concepts and activities through scenarios. This activity resulted in the creation of three different interactive prototypes that we tested with our informants.

Three new concepts

Oinkonomy

Oinkonomy is a digital concept where you take care of a virtual pig by managing your finances. The mood and home of your pig avatar reflect how well you're sticking to your predefined budget. You keep its spirits high by spending less in real life. If the mood is high, you gain more coins that you can use to assist your friends if they are having trouble maintaining their budget, or to buy new accesories and furniture for your pig's home. This creates a playful approach to personal and mutual economic understanding between friends. It also serves as a conversation starter around the taboo-filled topic, as users can relate to each other through the playful elements.

Quotes from participants

Alma, 25

University student

"It would make me think more about my spendings. I like the idea of nurturing or maintaining a pet and keeping it healthy and alive".

Carla, 26

University student

"You can start talking about these things, so I think it's a good conversation starter. It could make it less shameful.

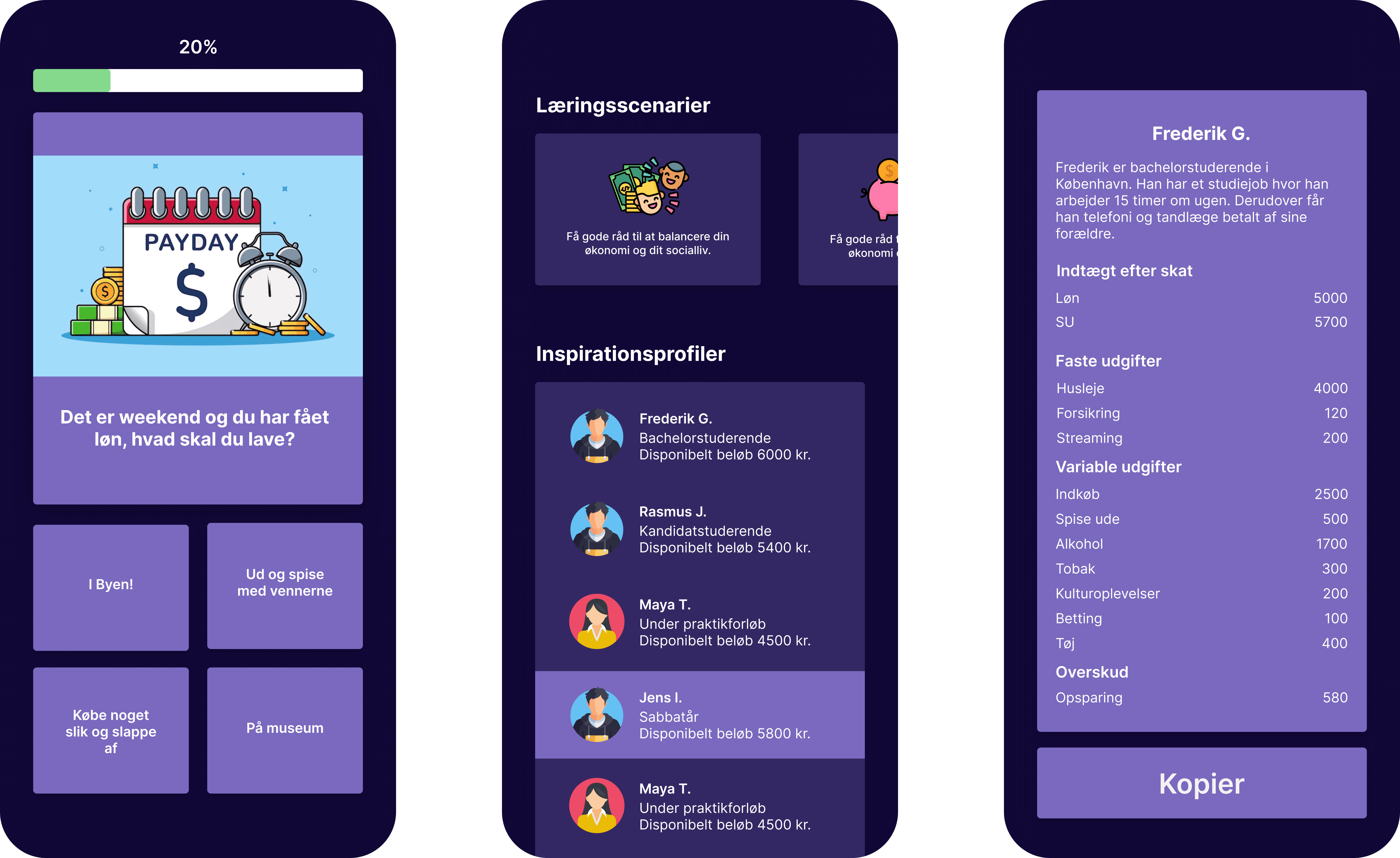

Peerconomics

With Peerconomics, the user can easily view and copy budgets from people with similar finances and life situations. Initially, users must answer questions about income, spending and financial goals. Users are suggested budgets and learning material based on the knowledge gathered about them. Users can then easily get an overview and insight into the finances of similar users and can copy other people's budgets.

Quotes from participants

"I like that you can look at others who have a similar profile and see what their budget is".

Carla, 26

University student

"You can read up on what they actually do and what they actually spend their money on. So you can compare yourself more 1 to 1".

"Now that it's an inspiration profile, you have to be inspired by others.

Budget Buddy

With Budget Buddy the user can set up individual budgets for different categories such as food, clothing and miscellaneous. Once this is done, the user can keep a continuous overview of their budgets in the form of Budget Buddy appearing as a widget on the user's home screen. When the user makes a purchase that falls under a budget that has already been exceeded, the user receives a notification that the budget has been exceeded. The user can now choose to confirm the purchase to complete it, or to decline the purchase and stay within their budget.

Test set-up and analysis

The trio of fresh ideas were subjected to a similar scrutiny as the original seven via think-aloud examinations and semi-formal discussions. For Budget Buddy though, we shifted to an in-situ approach, escorting our participants to a local supermarket. There, we tasked them with selecting specified items for their shopping cart and proceeding to the check-out point to scan them. Subsequently, they were handed a mobile with a notification from Budget Buddy, indicating this purchase would go beyond their budget limit. This practice offered a deeper colouring to our gathered data, since our intent was to reproduce an experience as close to real-life scenarios as possible.

Quotes from participants

Carla, 26

University student

"I like that you can get an overview of your usage and see how things are going without having to open an app. And it gives you a daily reminder".

"Really big fan of the fact that it's a widget - it kind of avoids it being just another app. So the biggest selling point is almost that it's a widget. It's really cool".

Alma, 25

University student

"Huge fan. I would love to have that widget (...) It could motivate, or I would just as much get satisfaction from being able to see that things are going as they should"

Deisgn guidelines

As the final deliverable of this research project, we have developed design guidelines based on self-determination theory. These guidelines are intended to serve as a starting point for future designers aiming to create digital tools that motivate young adults to become more financially literate. However, it is essential for future designers to conduct context-specific research to tailor these guidelines effectively.

Relatability:

Design guideline: The communication style of the design should neither talk down to nor go over the heads of young adults, but should meet them at eye level.

Potential risks: If the young adult is talked down to, this can minimize feelings of autonomy and competence

Relatability

Design guideline: The communication style of the design should neither talk down to nor go over the heads of young adults, but should meet them at eye level.

Potential risks: If the young adult is talked down to, this can minimize feelings of autonomy and competence

Competition

Design guideline: Gamification should only be used as a design tool to increase young people's intrinsic motivation by creating a sense of belonging among friends in social contexts.

Potential risks: This design tool can result in extrinsic motivation, as feelings such as vanity, shame, and loss of autonomy may arise.

Rewards

Design guideline: Symbolic rewards that communicate to the young adult that they have done well should result in an increased perception of competence.

Potential risks: Monetary rewards can result in extrinsic motivation.

Exposure of personal finance

Design guideline: Accessing other people's budgets should satisfy the individual's need for autonomy and competence

Potential risks: In this context, users should be anonymized as providing details about one’s personal finances can be sensitive information.

Guidance

Design guideline: When technology provides guidance in financial management, it should challenge young adults' skills appropriately.

Potential risks: If technology takes too much control over the young adult's financial decision-making, this can result in a sense of loss of control and lead to amotivation

Guidance

Design guideline: Financial management guidance must take into account the physical and temporal context of the young adult

Potential risks: If guidance is given at an inappropriate time while the young person is in a specific physical context, there is a risk that the young adult will prioritize other motivational factors over financial literacy

Relatedness with digital avatars

Design guideline: When the young adult's finances are represented by a digital personality, it should increase the sense of belonging and motivation to manage their finances

Potential risks: The representation can exploit the user's compassion and empathy, creating a guilty conscience or resulting in amotivation.